UPI Case Study: How India Built the World’s Largest Real-Time Payment Network

Home / Case Study / UPI Case Study: How India Built the World’s Largest Real-Time Payment Network

How did a payment system built in India go on to process nearly half of every real-time digital transaction on the planet? The answer has very little to do with a single clever app and almost everything to do with design: the way an entire financial network was structured, opened up, and scaled.

In the financial year 2025-26, the Unified Payments Interface (UPI) settled 24,162 crore transactions, roughly 241.6 billion payments, worth close to ₹314 lakh crore (Press Information Bureau, Government of India). That is not a startup success story. It is a national utility operating at a scale no private payment company has matched.

For a management student, UPI case study is one of the richest live case studies available. It sits at the intersection of platform strategy, operations, competitive dynamics, and international expansion. Study it closely and you learn how open ecosystems defeat closed ones, how systems absorb extreme demand without collapsing, and how a country can project economic influence through infrastructure rather than force.

What is UPI, and why should management students care?

UPI is India’s real-time, mobile-first payment system, and it belongs in a management classroom because it shows, at national scale, how a platform’s design decisions translate directly into market outcomes.

Most fintech platforms are judged by valuation, funding, or user growth. UPI is different because it was built as Digital Public Infrastructure (DPI): a shared, publicly governed rail that private companies build upon, rather than a private product that locks users in.

That single distinction explains almost everything that follows. Because the rail is open, hundreds of banks and dozens of apps plug into the same system. Because it is free for consumers to use, adoption exploded. And because no single company owns it, competition happens on top of the infrastructure instead of over it. These are the same themes explored in a PGDM programme, where strategy, finance, marketing, and operations meet in a single decision.

An everyday example: When you pay a vegetable vendor in your neighbourhood by scanning a QR code, tip a barber ₹50, or split a dinner bill with friends, you are using the same underlying rail that settles a corporate vendor payment. The vendor pays no card fee, you pay no transfer fee, and the money moves in seconds.

DID YOU KNOW?

UPI now handles roughly 49% of the world’s real-time payment transactions, more than three times the share of Brazil’s Pix, the next-largest system.

How did an open network dismantle the payment duopoly?

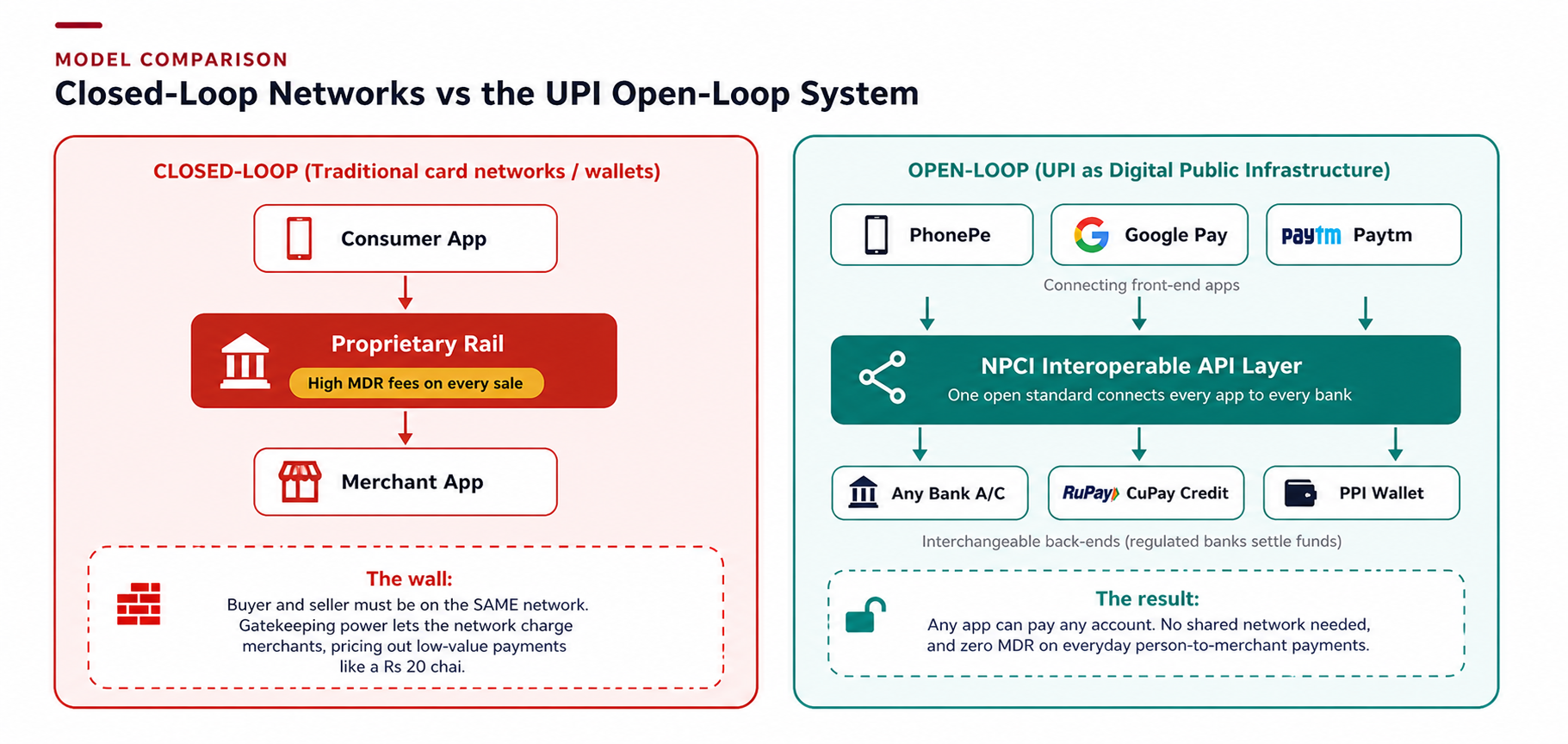

UPI broke the payment duopoly by removing the walls that closed networks depend on. To see why that matters, compare the two models.

In a closed-loop system, the customer and the merchant must both belong to the same network for a payment to work. Traditional card networks and wallets operate this way, and they use that gatekeeping position to charge merchants a Merchant Discount Rate (MDR) on every sale. For a shopkeeper selling a ₹20 cup of tea, a 2% fee is the difference between accepting a digital payment and refusing it. That friction is exactly why small merchants stayed cash-only for decades.

Figure 1. In a closed-loop network both parties must share a rail; UPI’s open-loop design lets any app pay any account with no MDR on everyday payments.

UPI took the opposite approach. Instead of building another walled garden, the National Payments Corporation of India (NPCI) built an open, interoperable layer that any bank and any app could join. The result is simple for the user and radical for the market: a PhonePe user can pay a Google Pay merchant, drawing from an account at one bank and depositing into an account at another, with no shared network required and no MDR on everyday person-to-merchant payments.

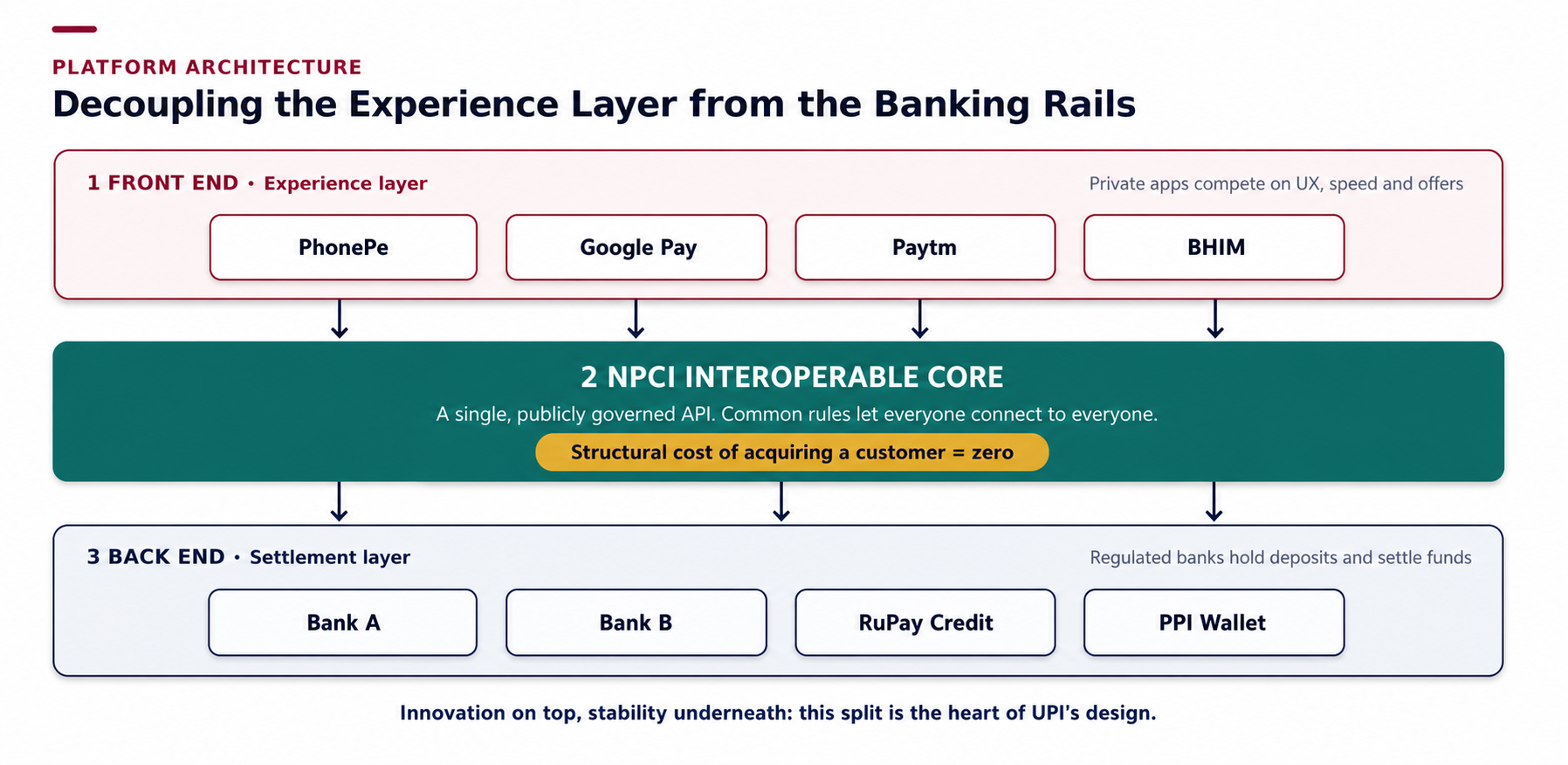

Why did separating the app from the bank change the game?

UPI separated the customer-facing app from the underlying banking system, and that structural split is the heart of its design. In plain terms, it let fintech companies focus on building a great user experience while banks kept doing what they do best: holding deposits and settling funds.

Think of it as two layers working together:

- The front end is where private companies compete. PhonePe, Google Pay, and Paytm fight for users through cleaner interfaces, faster onboarding, cashback offers, and reliability.

- The back end stays with regulated banks, which hold the actual money and complete each settlement quietly in the background.

Figure 2: UPI’s three-layer architecture: competing apps on top, a shared NPCI core in the middle, and regulated banks settling funds underneath.

Because these layers are connected by a common set of rules rather than owned by one company, a powerful multi-sided network effect took hold. This snowball is a classic study in marketing and platform strategy:

- Consumers joined because paying was free, instant, and worked on any phone.

- Merchants adopted UPI QR codes because they could not afford to turn away paying customers, and there was no fee to accept.

- That vast merchant footprint then pulled in even the most reluctant, late-adopting consumers.

By removing licensing barriers and network entry costs, UPI drove the structural cost of acquiring a customer close to zero, something no private fintech has been able to replicate.

Managerial insight

You do not always need to own the whole value chain to win. UPI created enormous private value by keeping the core rail open and public, then letting companies compete on the experience layer above it. For a strategist, the real question is which parts of your system should be shared standards and which should be points of differentiation.

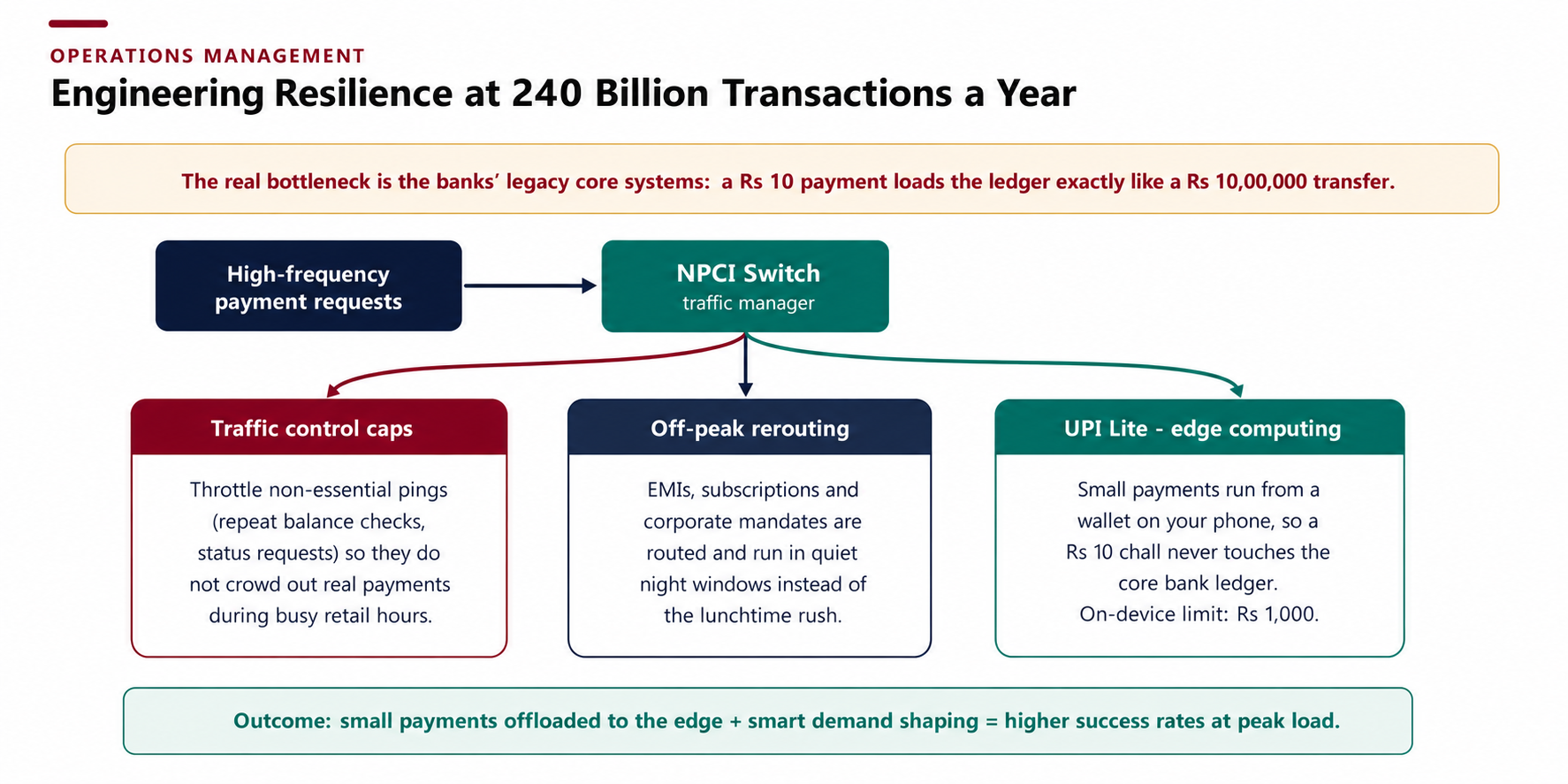

How does UPI stay stable while processing 240 billion transactions a year?

UPI stays stable by managing demand intelligently and pushing small payments away from the core banking systems, rather than relying only on bigger servers. Processing more than 240 billion transactions a year is an operations and capacity-management problem as much as a technology one, the kind tackled in a PGDM in Logistics and Supply Chain Management.

The critical insight is where the real pressure sits. It was never the central NPCI switch. The bottleneck has always been the ageing IT systems of individual banks. And here is the counter-intuitive part: a ₹10 payment puts the same computational load on a bank’s ledger as a ₹10,00,000 transfer. Millions of tiny payments can therefore congest the system just as badly as a few large ones.

Figure 3: Three operational levers keep success rates high at peak: throttling non-essential requests, rerouting recurring payments to off-peak windows, and moving micro-payments to on-device wallets.

To keep success rates high during peak hours, the ecosystem introduced three practical measures:

- Traffic control caps: The system now throttles non-essential requests, such as repeated balance checks and automated status pings, so they do not crowd out genuine payments during busy retail hours.

- Off-peak scheduling: Recurring payments such as EMIs, subscriptions, and corporate mandates are queued and processed during quiet night-time windows instead of competing with the lunchtime rush.

- UPI Lite (edge computing): Small payments run from a wallet stored directly on your phone, so a ₹30 chai does not need to touch the core banking ledger at all. The on-device wallet currently allows payments of up to ₹1,000 each (Reserve Bank of India, via DD News).

An everyday example: Buying a metro ticket or a plate of street food through UPI Lite clears almost instantly and never queues behind a bank server, because the payment happens on the device itself.

Managerial insight

You cannot scale purely by upgrading the central system. True scalability comes from shaping demand (managing when and how traffic arrives) and moving work to the edge (handling small tasks locally). The same principle governs cloud services, retail supply chains, and any high-volume operation.

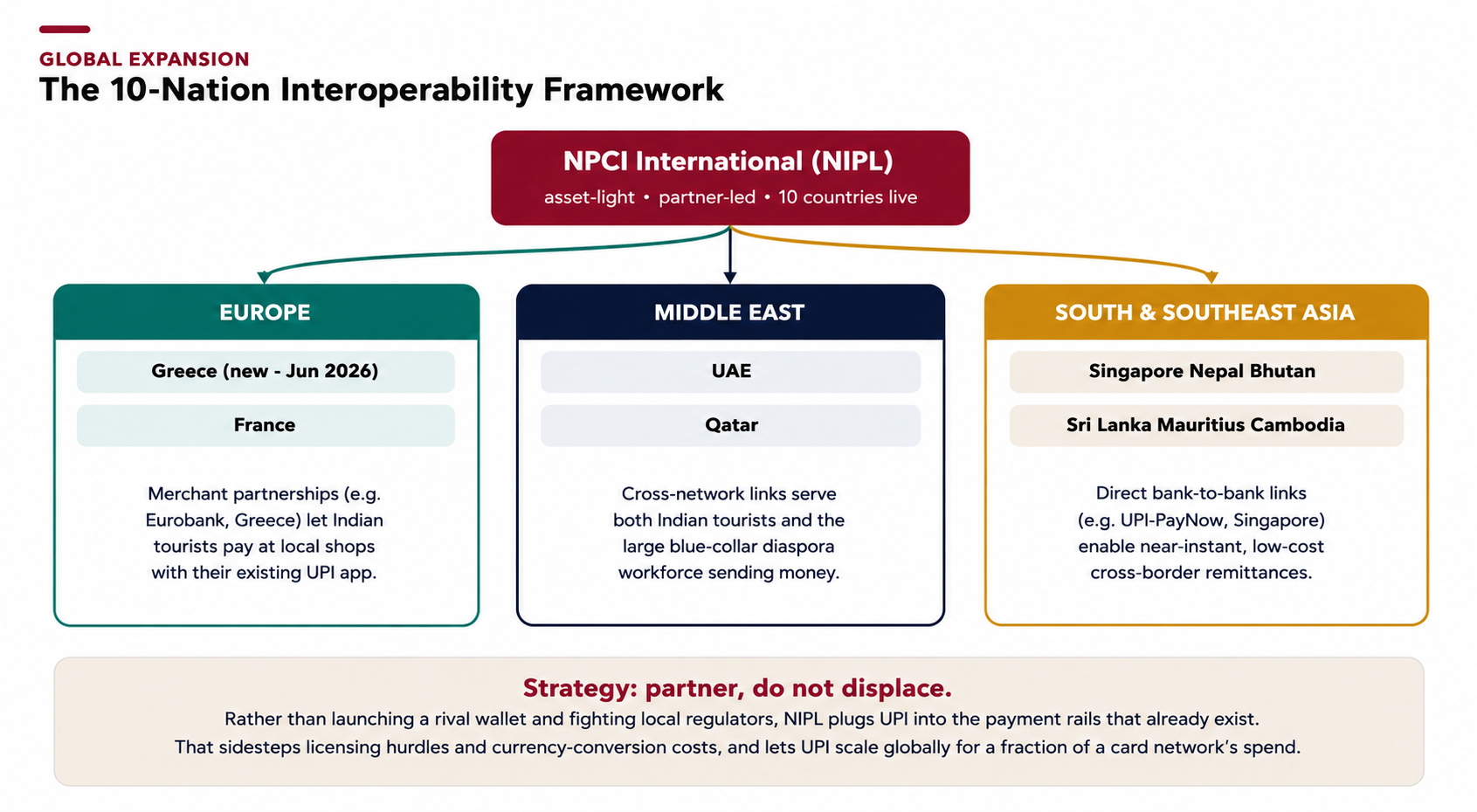

How is UPI scaling across borders without burning capital?

UPI is expanding internationally by partnering with existing local payment networks rather than building its own operations abroad. This asset-light strategy is run by NPCI International Payments Limited (NIPL). Instead of spending heavily to launch a rival wallet in each new country, NIPL plugs UPI into the rails that already exist there.

With Greece coming on board in June 2026, UPI is now accepted across ten countries (Business Today), grouped into three broad corridors.

Figure 4. NIPL’s partner-led model now spans ten countries across Europe, the Middle East, and South and Southeast Asia.

| Corridor | Countries enabled | How it works |

|---|---|---|

| Europe | Greece (newest, June 2026) France |

Merchant partnerships (for example, Eurobank in Greece) let Indian tourists pay at local shops using their existing UPI app. |

| Middle East | UAE, Qatar | Cross-network links serve both Indian tourists and the large blue-collar diaspora workforce sending money home. |

| South and Southeast Asia | Singapore, Nepal, Bhutan, Sri Lanka, Mauritius, Cambodia | Direct bank-to-bank linkages, such as the UPI-PayNow link with Singapore, enable near-instant cross-border remittances. |

An everyday example: An Indian tourist can now scan a QR code near the Eiffel Tower in Paris or at a shop in Athens and pay directly from a bank account back home, with no foreign card and no currency-exchange counter.

The strategy is deliberate. Rather than fighting local regulators and incumbents, NIPL partners with national banks and dominant local switches. That approach sidesteps complex local licensing, avoids heavy currency-conversion costs, and lets UPI expand for a fraction of what a traditional card network would spend.

Managerial insight

You cannot scale purely by upgrading the central system. True scalability comes from shaping demand (managing when and how traffic arrives) and moving work to the edge (handling small tasks locally). The same principle governs cloud services, retail supply chains, and any high-volume operation.

Is UPI quietly reshaping global financial power?

Yes, in a modest but real way, UPI is beginning to reshape how money moves between countries, chiefly by reducing dependence on the traditional dollar-based settlement network. For students of finance, this is where payments meet geopolitics.

Bypassing the dollar-clearing chain

For decades, a cross-border payment from, say, Mumbai to Athens has typically been converted into US dollars or euros and routed through Western correspondent banks over the SWIFT network. Each hop adds fees, and settlement can take several days.

By building direct, bilateral corridors, UPI allows two countries to settle in their own currencies, in real time, bypassing that dollar-clearing chain. For participating nations, this reduces dependence on Western financial infrastructure, lowers exposure to unilateral sanctions, and keeps more liquidity inside the local economy.

Returning money to families

There is a second, very human dimension: remittances. India has been the world’s largest recipient of remittances since 2008 (World Bank). Historically, sending money home has cost migrant workers dearly. The global average cost of a remittance is still around 6.4%, and can run higher through banks; the United Nations’ Sustainable Development target is to bring it below 3%.

By linking real-time retail payment systems directly, UPI pushes cross-border transfer costs toward a fraction of the traditional rate, meaning more of a worker’s money reaches their family instead of being eaten by fees.

Did you know?

A worker who pays 6% in fees loses ₹600 on every ₹10,000 sent home. Across the billions of dollars India receives each year, shaving even a few percentage points returns enormous sums to household incomes.

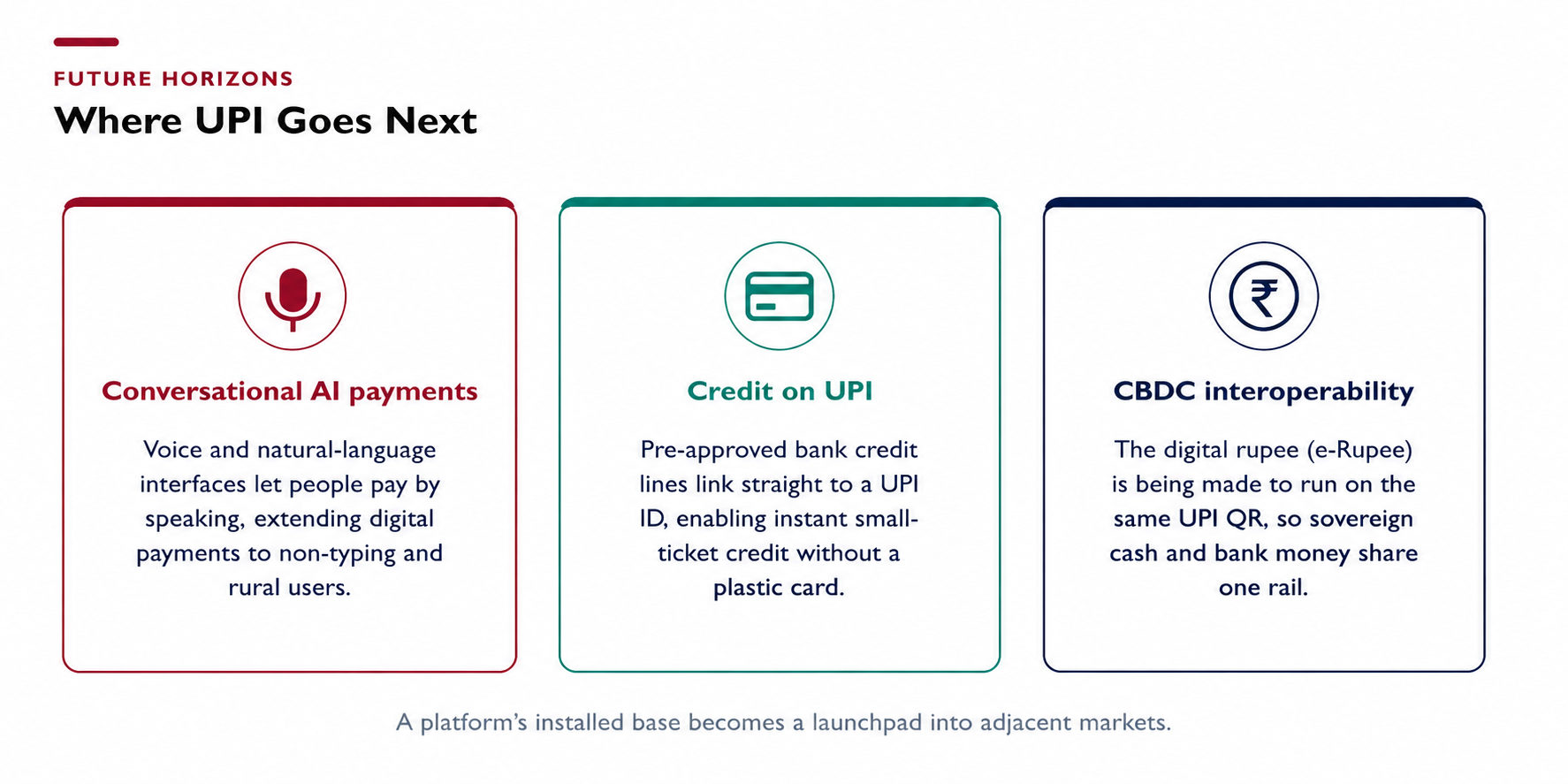

What comes next for UPI?

UPI’s next phase focuses on three frontiers: conversational payments, credit, and digital currency. Each extends the system into new territory, building on the enormous base it has already installed.

Figure 5. Three frontiers for the next decade of UPI: voice-driven payments, credit delivered without a card, and interoperability with the digital rupee.

- Conversational, AI-driven payments. Voice-based, natural-language interfaces will let people pay by simply speaking, extending digital payments to users who are not comfortable with typing and deepening reach in semi-urban and rural India.

- Credit on UPI. Banks can now link pre-approved credit lines directly to a user’s UPI ID, letting people spend on credit without a physical card. This turns UPI into a channel for instant, small-ticket credit and challenges the traditional credit-card model.

- Digital rupee (CBDC) integration. The central bank’s digital currency, the e-Rupee, is being made interoperable with UPI QR codes, so sovereign digital cash and ordinary bank money can run on the same rail and the same QR sticker.

Taken together, these signal how digital commerce evolves once a payment rail becomes ubiquitous. They are a natural focus for IMT Hyderabad’s Centre for Digital Transformation.

Managerial insight

A successful platform does not stop at its first use case. UPI is using its installed base as a launchpad for credit, voice commerce, and digital currency. For future managers, the lesson is that distribution, once built, becomes a strategic asset you can extend into adjacent markets.

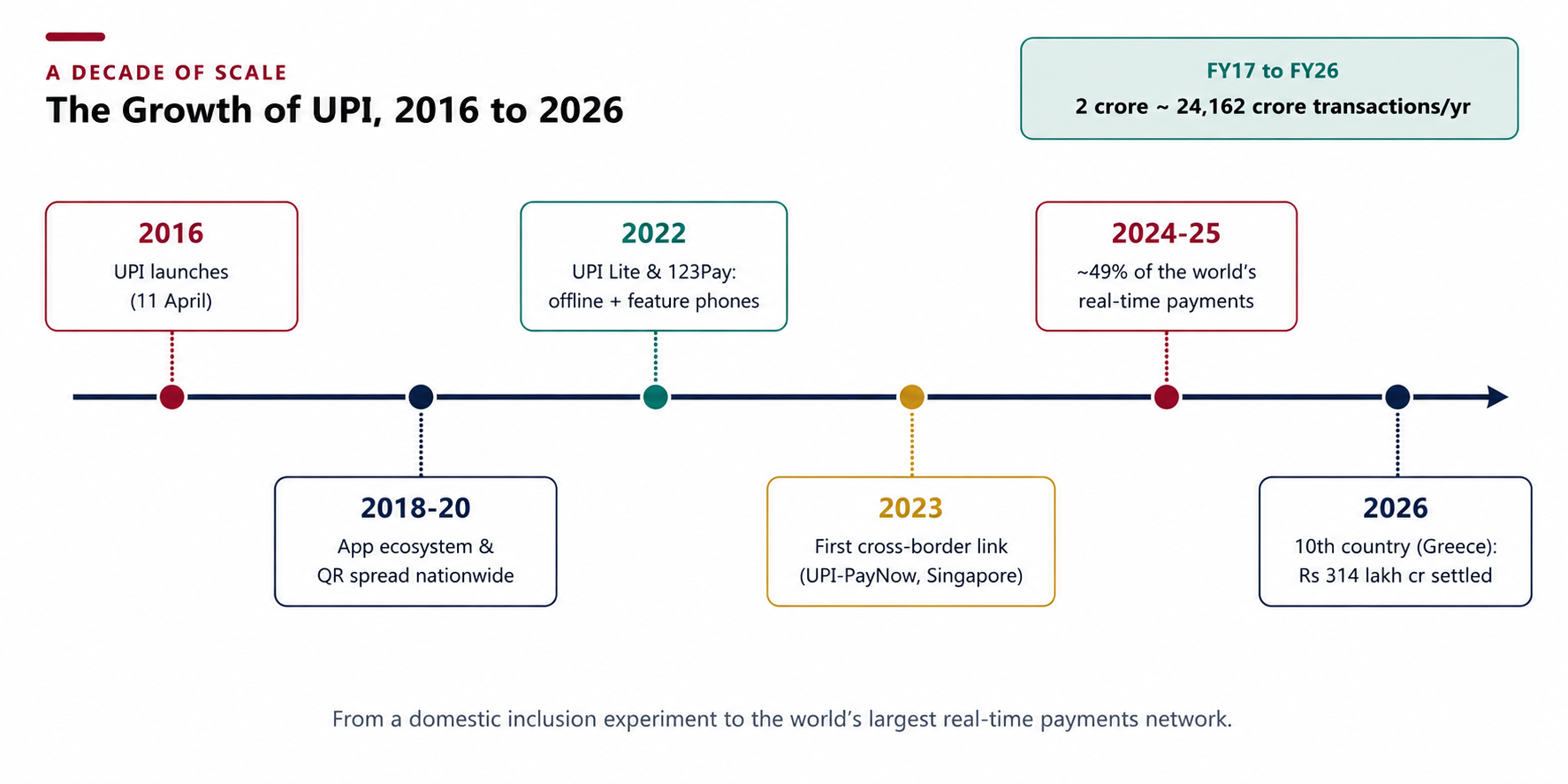

The journey at a glance

Figure 6: From a domestic inclusion experiment in 2016 to the world’s largest real-time payments network a decade later.

What can future managers learn from UPI?

UPI’s real lesson is not about payments at all. It is about how to design systems that scale. For the next generation of business leaders, three ideas stand out.

- Public infrastructure can create private wealth. By treating the core rail as a shared utility, India built an open ecosystem where private companies could innovate on a stable foundation, driving efficiency across the whole economy.

- Scale is an act of design, not just of spending. High-volume systems survive by shaping demand and moving work to the edge, not merely by buying bigger servers.

- Collaboration can outperform disruption. In new markets, partnering with existing networks opens a faster, cheaper path to scale than trying to displace them.

Ultimately, UPI shows that the future belongs to open, interoperable, asset-light platforms. The takeaway for tomorrow’s managers is clear: do not just build a better product. Aim to design a better ecosystem.

Key takeaways

- Open beats closed. Removing network walls and MDR unlocked a merchant and consumer network effect that no closed system could match.

- Decoupling drives competition. Splitting the experience layer from the settlement layer let apps innovate while banks stayed stable.

- Scale is engineered. Traffic shaping and edge processing (UPI Lite) protect the system at 240 billion-plus transactions a year.

- Partner, do not displace. An asset-light, partner-led model carried UPI to ten countries at low cost.

- Distribution is a launchpad. Credit, voice, and the digital rupee all ride on the base UPI has already built.

Related Blogs

The Apple Comeback Under Tim Cook: A Business Case Study for PGDM Courses and Future Managers

Summary When Tim Cook became chief executive of Apple in 2011, many people doubted that…

How Reliance Jio Revolutionized India’s Telecom Industry: Strategic Lessons for PGDM Students

Summary This case study examines how Reliance Jio transformed India’s telecommunications industry within a few…

Pepsi Vs Coca-Cola: The Cola Wars and What They Teach Future Business Leaders

Summary The rivalry between Pepsi and Coca-Cola, widely known as the Cola Wars, is one…

How Titan Became One of the World’s Largest Watch Manufacturers

Summary This case study examines how Titan, a joint venture between the Tata Group and…