Zepto vs Blinkit vs Instamart: A Strategic PGDM Case Study of India’s Quick Commerce Revolution

Home / Case Study / Zepto vs Blinkit vs Instamart: A Strategic PGDM Case Study of India’s Quick Commerce Revolution

Why is India’s quick commerce revolution worth studying?

Quick commerce is the fastest-adopted retail format in modern Indian history, and five years ago it did not exist at meaningful scale. The category, namely the delivery of groceries and daily essentials in ten to twenty minutes from small neighbourhood warehouses, moved from an unproven experiment to an estimated 11billion US dollars in annual gross merchandise value during 2025, and is widely forecast to multiply several times over by 2030.

Three companies define the contest, and studying them together is valuable because each represents a distinct answer to a single, unforgiving question: how do you build a profitable business on a promise as expensive as instant delivery?

- Blinkit, owned by the listed company Eternal (formerly Zomato), is the market leader and the first player to prove the model can make money, through operating discipline and inventory control.

- Zepto, the youngest of the three and the only large independent pure-play, has grown at a breathtaking pace and filed to go public in 2026.

- Swiggy Instamart, the quick commerce arm of listed food-delivery company Swiggy, pioneered the category alongside the others but has lately been squeezed on both growth and market share.

This Zepto vs Blinkit vs Instamart case study traces those choices through business models, dark store operations, technology, marketing and, above all, the unit economics that will decide who survives the arrival of Flipkart and Amazon.

Figure 1. The competitive map: only Blinkit sits above the break-even line (FY26).

How did quick commerce evolve in India?

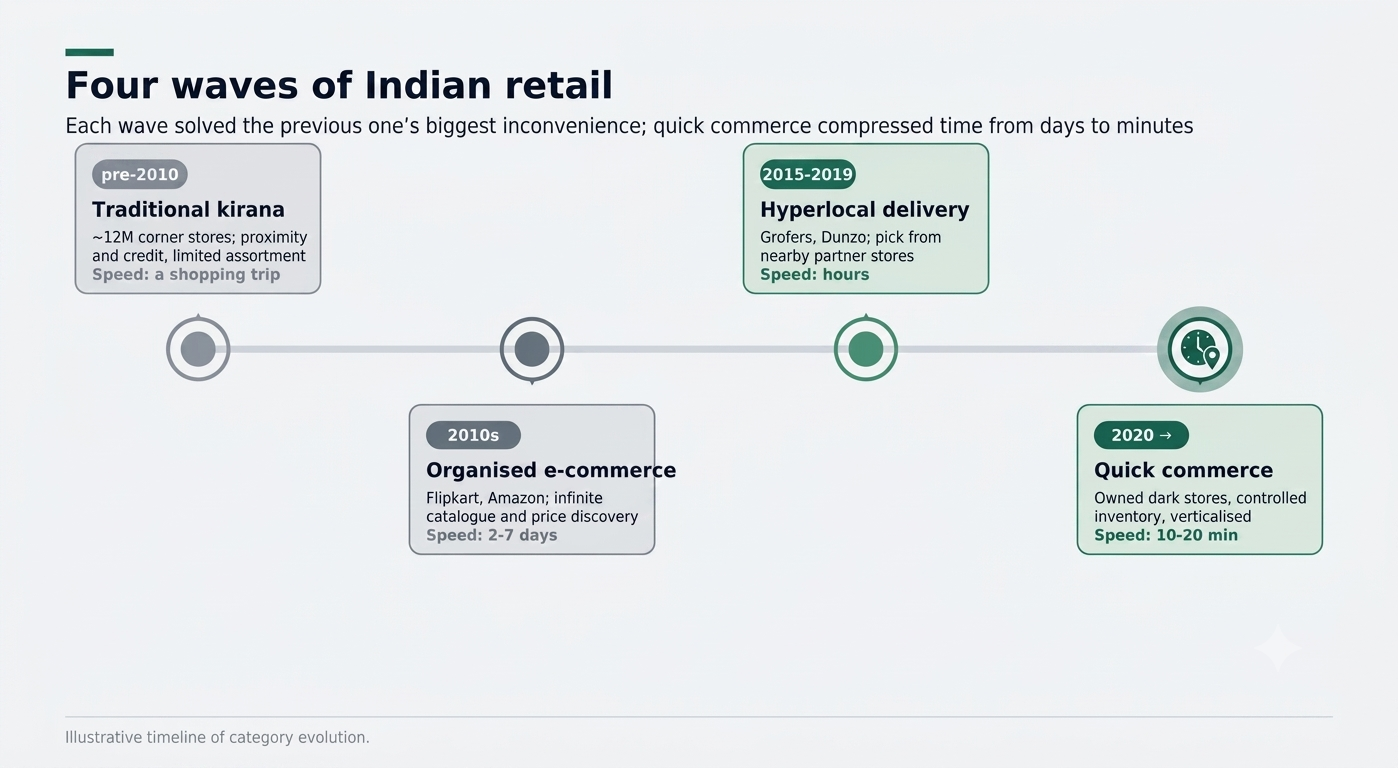

Quick commerce is the fourth stage in a two-decade migration of Indian retail from the corner shop to the smartphone, and each stage solved the previous stage’s biggest inconvenience.

- Traditional kirana (pre-2010): roughly twelve million small stores offered unmatched proximity and personal credit, but limited assortment and no digital footprint.

- Organised e-commerce (2010s): Flipkart and Amazon solved assortment and price discovery with near-infinite catalogues, yet delivered over days, not minutes.

- Hyperlocal delivery (2015 to 2019): the early Grofers, Dunzo and others compressed delivery to hours by picking from partner stores, inheriting messy economics.

- Quick commerce (2020 onward): operators built their own dense network of dark stores and controlled inventory directly, collapsing delivery to ten to twenty minutes.

Two forces made the timing right. On the demand side, the pandemic normalised online grocery and reset expectations, so a generation of urban consumers came to treat instant delivery as a default rather than a luxury. On the supply side, cheap micro-warehouse real estate, an abundant gig workforce and mature UPI payments removed the practical barriers. Crucially, quick commerce did not simply digitise existing demand; it created new, small, frequent, impulse-led orders that consumers would previously never have made a dedicated trip for.

Figure 2. Four waves of Indian retail, and the compression of delivery time.

Who are the three contenders?

The three leaders differ not only in scale but in ownership structure, capital access and strategic personality, and those differences explain much of their behaviour.

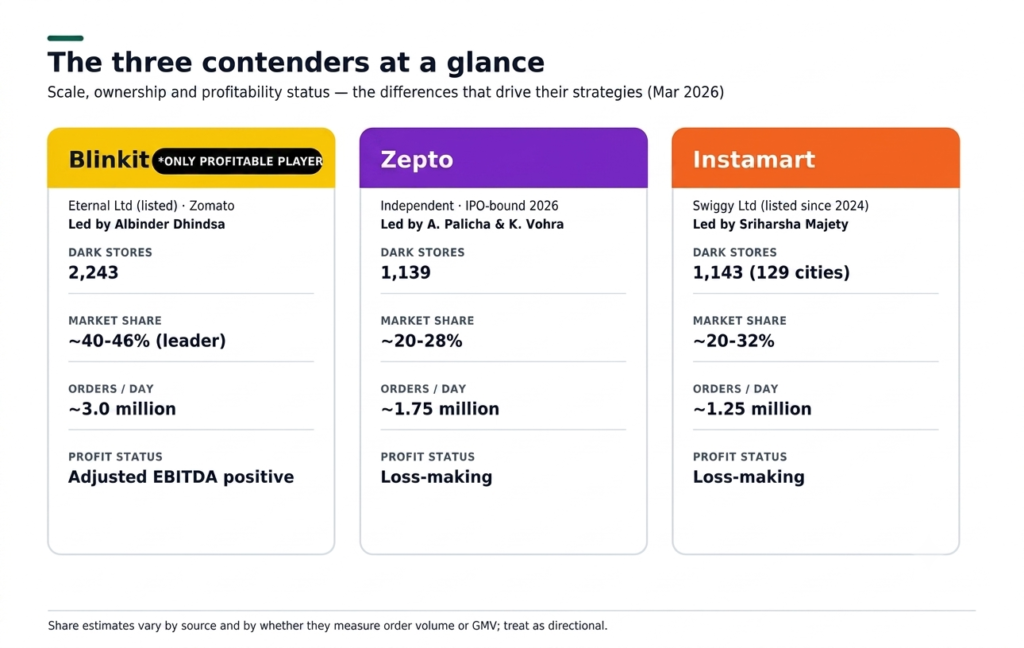

Blinkit began in 2013 as Grofers, founded by Albinder Dhindsa and Saurabh Kumar, rebranded to Blinkit in December 2021 and was acquired by Zomato in 2022. It now operates as the quick commerce division of Eternal Limited. Positioned around premium groceries and reliable replenishment, it reached 2,243 dark stores by March 2026 and an estimated 40-46% of the market, the widest network and the strongest data and advertising tools in the category.

Zepto was founded in 2021 by Aadit Palicha and Kaivalya Vohra, childhood friends who dropped out of Stanford at nineteen. Headquartered in Mumbai, it is the only large pure-play operator and the youth-first brand, backed by investors including Y Combinator, Lightspeed and, in October 2025, the US pension fund CalPERS. It reached roughly 1,139 dark stores and around 48 million annual transacting users in FY26 and filed to list publicly in 2026.

Swiggy Instamart launched in 2020 as the quick commerce service of Swiggy, which was founded in 2014 and listed in November 2024. Listing gave Instamart the balance-sheet backing of a diversified platform and deep overlap with Swiggy’s food-delivery base. Positioned around meal- and kitchen-adjacent essentials, it operated 1,143 dark stores across 129 cities by March 2026, but its market share has slipped as rivals expanded faster.

| Force | Intensity | Why it matters for strategy |

|---|---|---|

| Competitive rivalry | Very high | Three funded incumbents plus two global entrants; metro capacity is already oversupplied, sustaining a price war. |

| Threat of new entry | High and rising | Flipkart and Amazon bring deep capital and logistics scale, neutralising the capital barrier that once protected incumbents. |

| Buyer power | High | Near-zero switching costs; multi-homing consumers chase the best deal, keeping discounting alive and margins thin. |

| Supplier power | Moderate | Owned inventory and private labels reduce brand leverage, but scarce gig labour and regulation raise delivery cost. |

| Threat of substitutes | Moderate | Kirana, scheduled e-commerce and planning ahead all substitute; instant delivery is attractive, not essential. |

Table 1. Company snapshot: Share estimates vary by source and by whether they measure order volume or GMV.

Figure 3. The three contenders at a glance.

How do their business models compare?

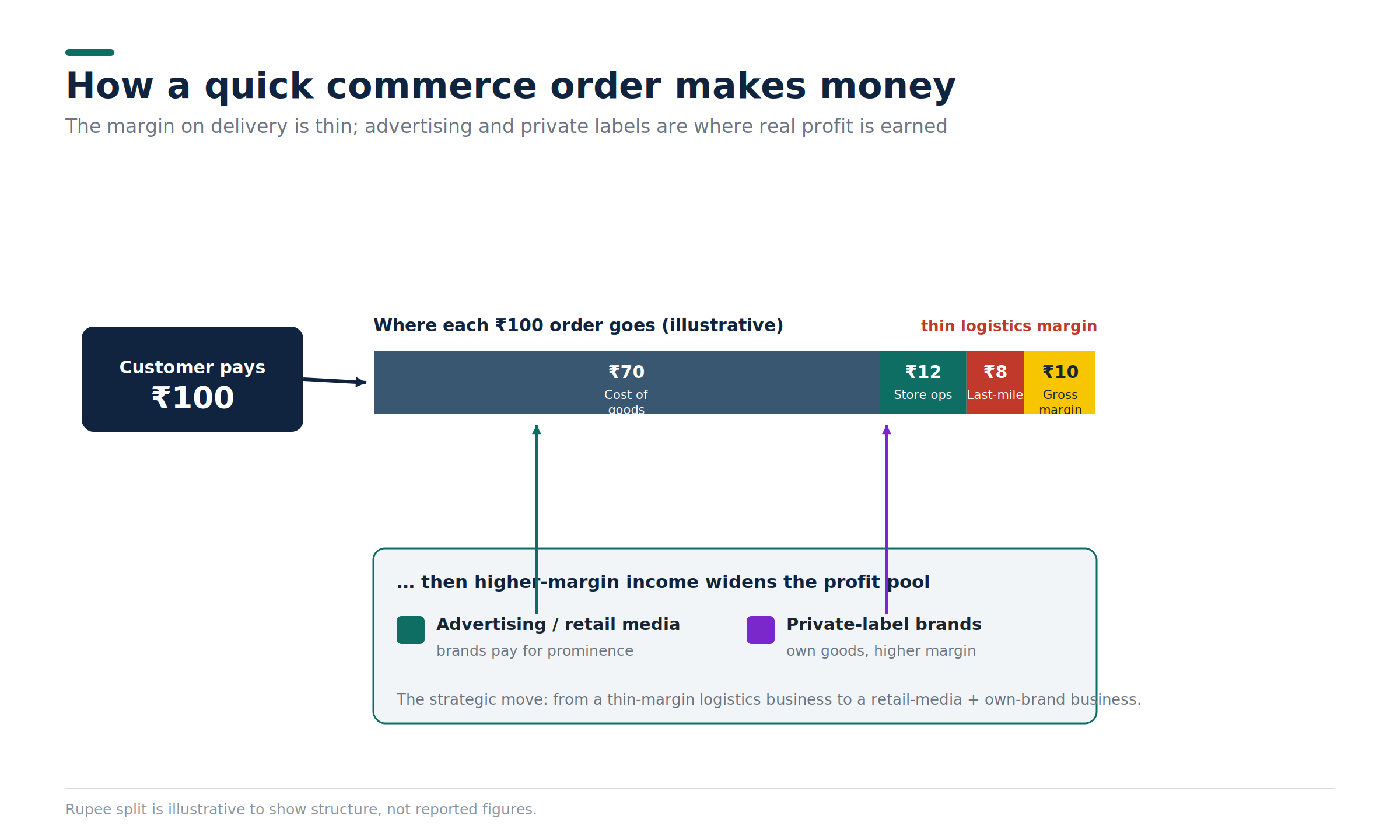

All three earn money the same way in principle, but the mix of streams and the underlying inventory model differ in ways that materially change reported economics. Revenue comes from four levers.

- Product margin: the gap between the supplier price and the customer price, plus commission on branded goods. This is the core engine.

- Delivery and handling fees: small charges that flex with order size, distance, weather and time, and are waived above a minimum basket.

- Advertising and retail media: the fastest-growing and most profitable stream. Zepto’s advertising revenue grew more than 151 per cent year on year to about 1,640 crore rupees in FY26, outpacing its core revenue.

- Subscriptions and private labels: paid passes such as Zepto Pass lock in frequency, while own-brands lift margin and reduce dependence on third-party brands.

A pivotal structural choice separates the leaders. Blinkit moved during FY26 from a marketplace model, in which it earned only a commission, to an inventory-led model, in which it owns the goods and books their full value as revenue. By late in the year roughly ninety per cent of its order value ran through owned inventory. This is why its headline revenue appears to leap, and why Net Order Value is the cleaner measure. The strategic logic across all three is identical: move from a thin-margin logistics business toward a higher-margin retail-media-and-owned-brand business.

| Revenue lever | Blinkit | Zepto | Swiggy Instamart |

|---|---|---|---|

| Inventory model | Inventory-led (~90% of NOV) | Verticalised, owned inventory | Inventory-led |

| Product margin | Core | Core | Core |

| Delivery / handling fees | Yes; free above minimum basket | Yes; free above minimum basket | Yes; no-fee campaign rolled back Jan 2026 |

| Advertising / retail media | Most mature tools | Fast-growing (+151% in FY26) | Swiggy Ads integration |

| Subscription | Paid tier | Zepto Pass | Swiggy One overlap |

| Private labels | Expanding | Staples, fresh, home care | Growing |

| Adjacencies | Bistro / ready food | Zepto Café; Zepto Nova | Swiggy food-delivery cross-sell |

Table 2. Revenue architecture. NOV is Net Order Value, the more comparable measure than headline revenue after the shift to inventory-led accounting.

Figure 4. Where each rupee of an order goes, and how advertising widens the profit pool.

How does the dark store model actually work?

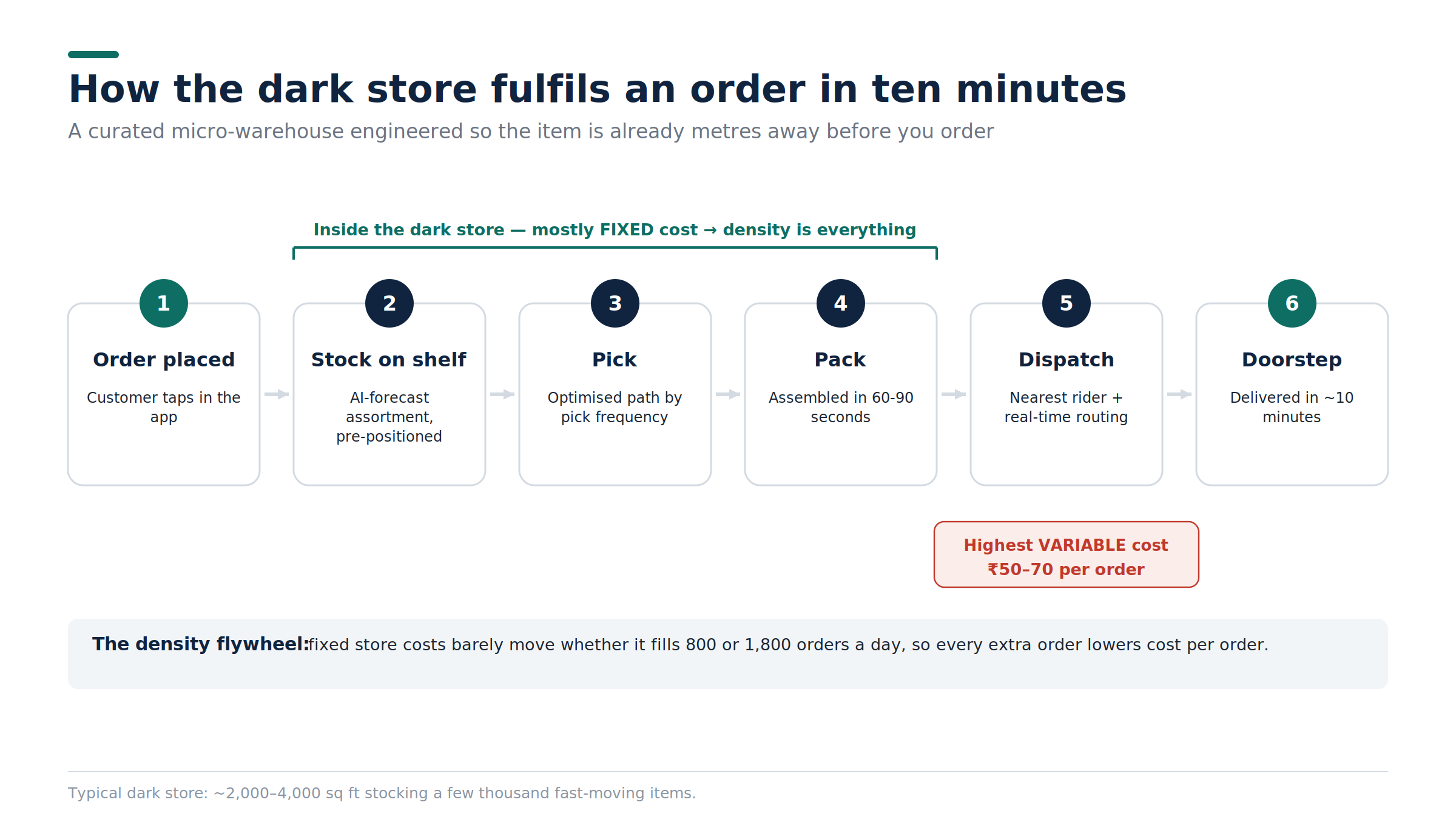

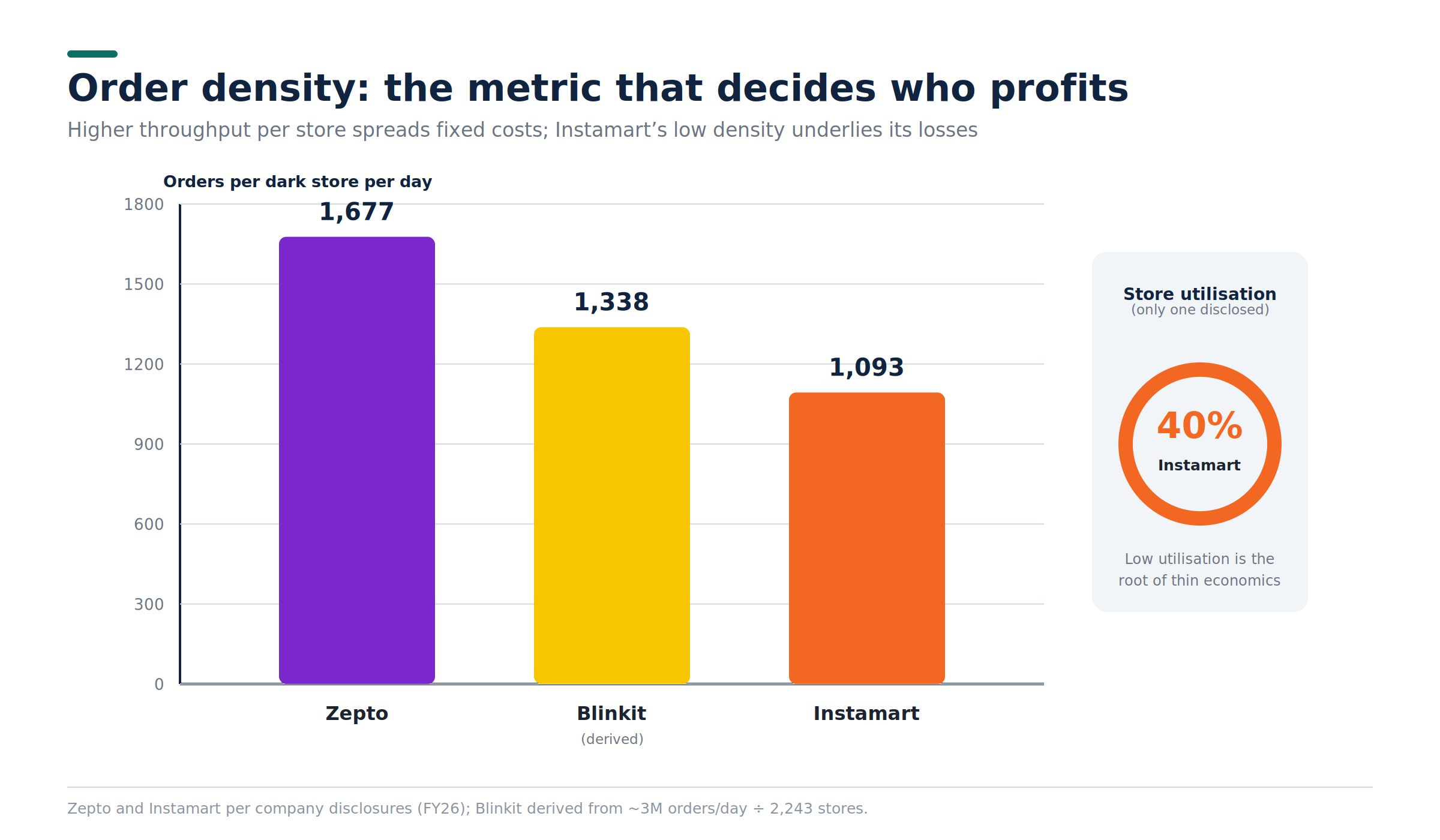

A dark store is a small, windowless micro-warehouse, typically two thousand to four thousand square feet, that stocks a few thousand of the fastest-moving items and exists purely to fulfil online orders. Its entire economic logic rests on one number: orders per store per day.

- Placement: because a rider must arrive in ten minutes, each store serves a tight radius of dense demand, chosen with granular data and geospatial heat maps. The model thrives in metros and struggles where density is thin.

- Inventory: a curated assortment of high-velocity products is held close to the customer, with machine-learning forecasts deciding what each individual store stocks.

- Pick and pack: items are arranged by picking frequency, staff follow optimised pick paths, and an order is assembled in roughly sixty to ninety seconds.

- Last-mile delivery: the largest single cost, at roughly fifty to seventy rupees per order, assigned to the nearest rider with real-time route optimisation.

The reason this configuration matters is the density flywheel. A store’s major costs, namely rent, staff and equipment, are largely fixed, so whether it fulfils eight hundred orders a day or eighteen hundred, that base cost barely moves. Every additional order spreads the same fixed cost over a larger base. Zepto, for example, averaged roughly 1,677 orders per store per day in FY26, up from about 1,325 two years earlier; Instamart, by contrast, was running near 1,093, which is a large part of why its store-level economics remain weaker.

Figure 5. How a dark store fulfils an order in ten minutes.

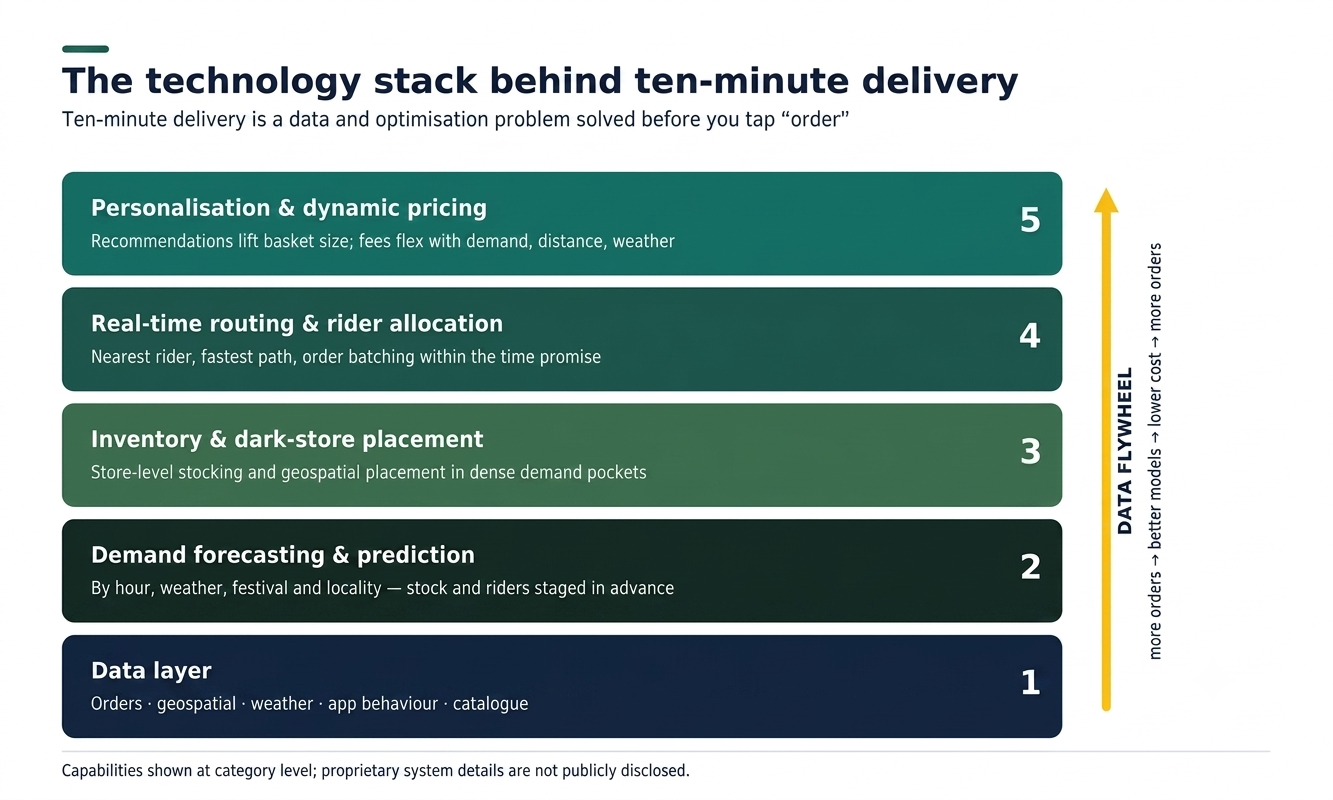

What technology powers ten-minute delivery?

Ten-minute delivery is fundamentally a data and optimisation problem solved before the customer taps order, not a heroics problem solved after, and artificial intelligence sits at every decision point in the chain.

- Demand prediction and heat maps: decide where stores go and what they hold, forecasting down to the individual store and product.

- Inventory and replenishment: keep shelves accurate in real time, minimising both stockouts, which lose the sale, and overstocking of perishables, which destroys margin.

- Recommendations: raise average order value by turning a single-item impulse into a larger basket.

- Routing and rider allocation: assign the best-placed rider and compute the fastest path, batching nearby orders without breaching the promise.

- Dynamic pricing: delivery and handling fees flex with demand, distance, weather and rider supply to protect economics during peaks.

The strategic point for managers is that technology here is the core of the operating model, not a support function. The same forecasting engine that improves customer experience also drives the density flywheel, because better prediction means fuller stores, tighter picking and more efficient routing. Scale compounds the advantage: the leader with the most orders generates the most data, which sharpens its models, which improves its economics, which funds further expansion.

Figure 6. The technology stack behind ten-minute delivery.

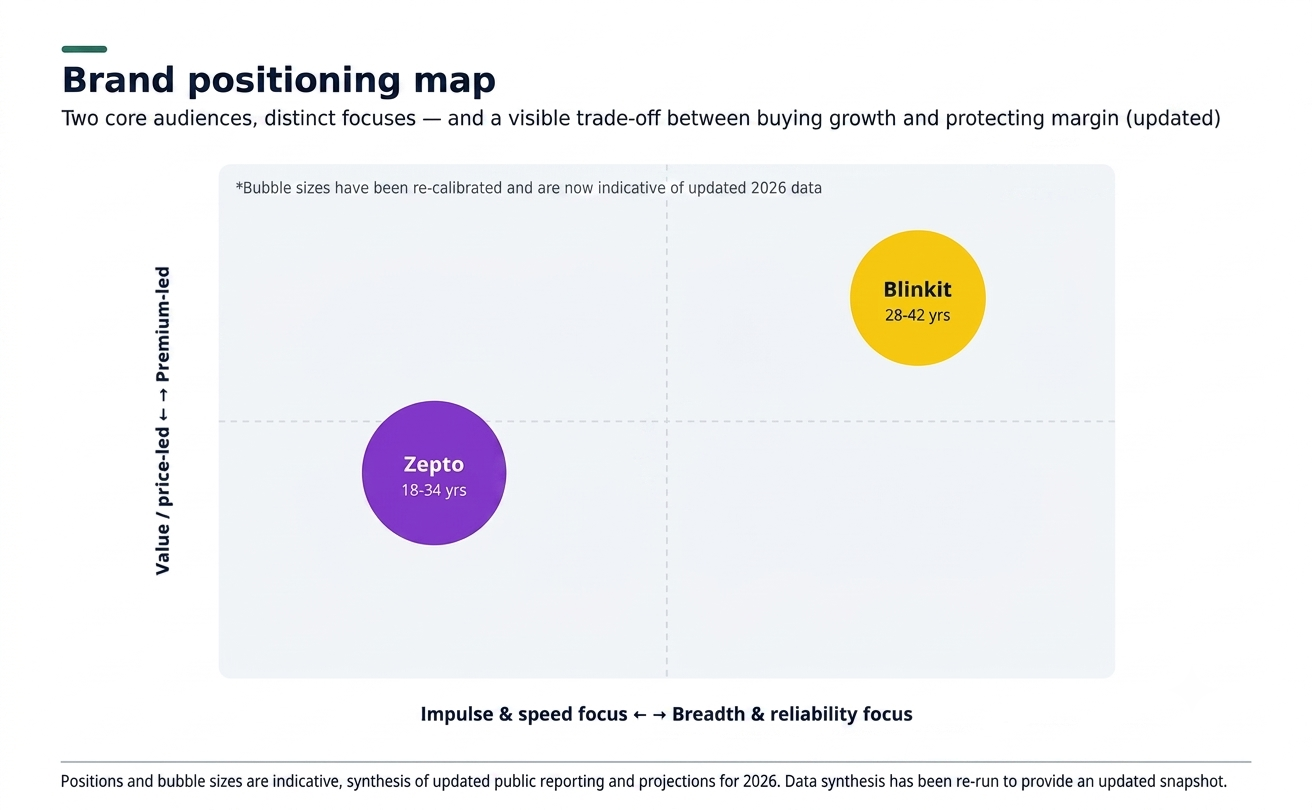

How do their marketing strategies differ?

The three brands compete for different consumers with different messages, and their marketing choices flow directly from their strategic positioning rather than from generic category advertising.

- Blinkit targets the urban premium household, roughly twenty-eight to forty-two, and sells reliability and breadth, supported by sharp, topical real-time marketing.

- Zepto targets Gen Z and younger millennials, roughly eighteen to thirty-four, and sells speed and impulse through fast, culturally fluent social campaigns.

- Instamart targets meal-oriented families and leans on Swiggy’s heritage and cross-promotion.

Customer acquisition has, until recently, been fuelled by heavy discounting across all three, a costly lever that inflates growth but erodes margin, which is precisely why Blinkit has publicly criticised aggressive discounting as poor-quality growth. Loyalty programmes are increasingly the retention engine, trading a discount for durable frequency. Pricing has become a battleground of its own: Instamart ran and then withdrew a no-fee campaign in January 2026, a decision that shows how finely balanced growth and margin have become, while new entrant Flipkart deploys some of the deepest discounts in the market to buy share.

| Dimension | Blinkit | Zepto | Swiggy Instamart |

|---|---|---|---|

| Core audience | Urban premium, 28–42 | Gen Z / millennial, 18–34 | Meal-oriented families, 25–45 |

| Brand promise | Reliability and breadth | Speed and impulse | Food- and kitchen-first |

| Acquisition style | Efficiency-led; anti-deep-discount | High-energy, viral, trial-driven | Swiggy cross-promotion |

| Social media | Topical real-time marketing | Culturally fluent, youth-native | Leverages Swiggy equity |

| Loyalty | Paid tier | Zepto Pass | Swiggy One overlap |

| Pricing posture | Protect margin | Aggressive on speed and trial | Withdrew no-fee campaign, Jan 2026 |

Table 3. Marketing and positioning at a glance.

Figure 7. Brand positioning map.

How efficient are their operations and supply chains?

Operational efficiency in quick commerce reduces to converting fixed dark store capacity into the highest possible order throughput at the lowest cost per order, and the three players sit at visibly different points on that curve.

- Utilisation: Blinkit’s mature markets such as Delhi NCR already approach a five to six per cent adjusted EBITDA margin, so profitable mature stores subsidise the ramp-up of new ones. Instamart reported dark store capacity utilisation of around forty per cent in early 2026, the operational root of its continuing losses.

- Inventory turnover: curated fast-movers and store-level forecasting mean inventory turns quickly, working capital is efficient and payment cycles are short with no credit risk.

- Delivery fleet: all three depend on large gig-worker fleets. Swiggy saw its monthly transacting delivery partners fall meaningfully in early 2026 even as orders grew, a supply-demand mismatch that pressures either delivery times or rider earnings.

- Cost efficiency: Blinkit credited its move into profit to supply-chain efficiencies, a favourable shift toward long-tail higher-margin categories, operating leverage and the benefit of owning inventory.

Figure 8. Order density per store, the metric behind who profits.

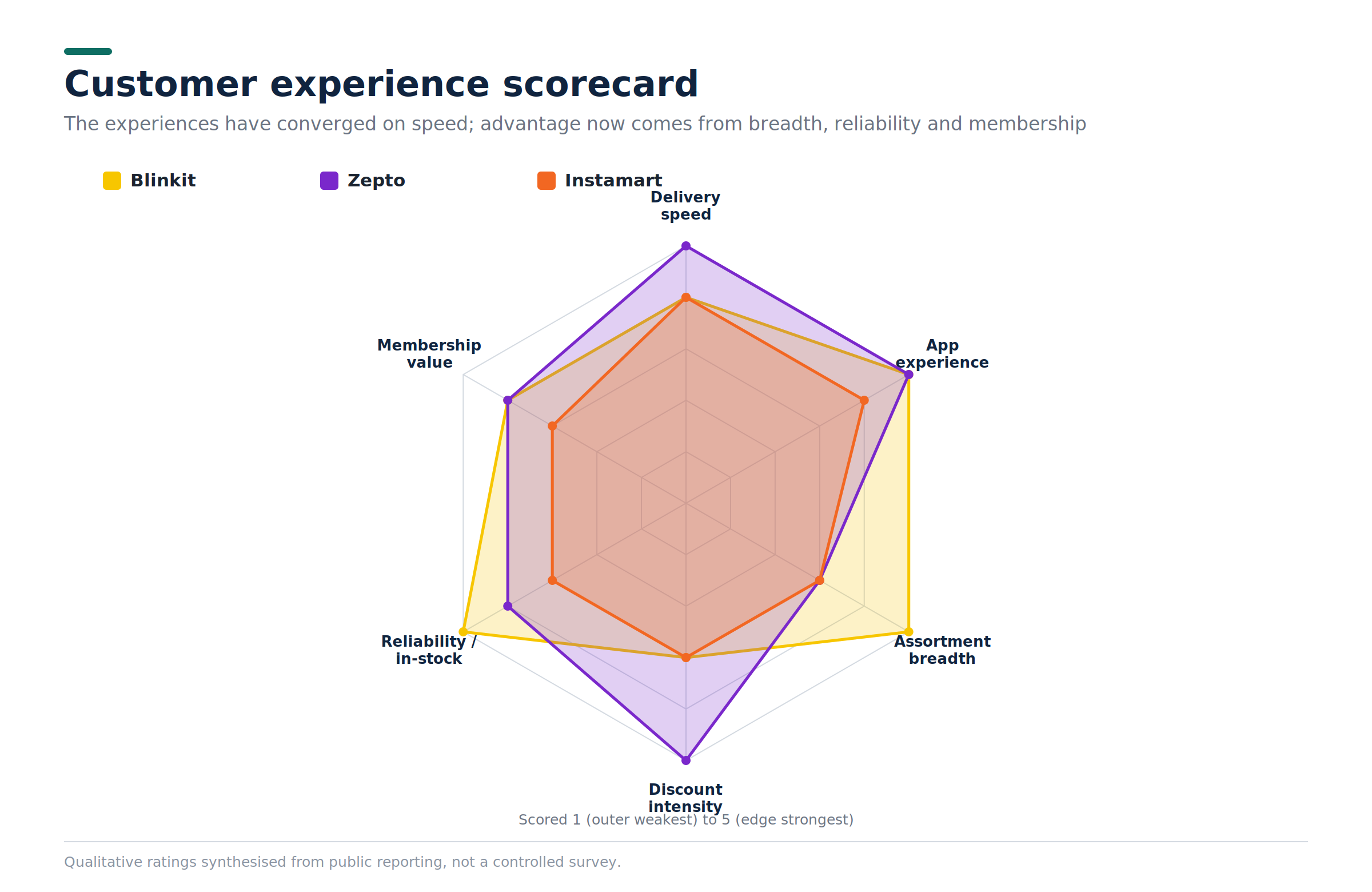

Which platform delivers the best customer experience?

For most everyday orders the three experiences have converged, so differentiation now comes from assortment depth, reliability and membership value rather than from raw speed, which all three deliver.

- Speed and app experience: broadly at parity; each delivers within ten to twenty minutes with a polished interface, so the marginal minute is no longer decisive.

- Assortment: Blinkit’s larger stores lead on breadth, especially premium and long-tail; Zepto is strongest in snacks, beverages and new-launch impulse products; Instamart is strongest in kitchen and meal-adjacent goods.

- Discounts: still a genuine driver, so whoever runs the most aggressive promotion often wins the marginal order, which keeps discounting intensity high.

- Reliability and membership: in-stock rates and accurate delivery separate a loyal customer from a churned one, and paid passes convert occasional users into high-frequency ones, lifting lifetime value.

Figure 9. Customer-experience scorecard.

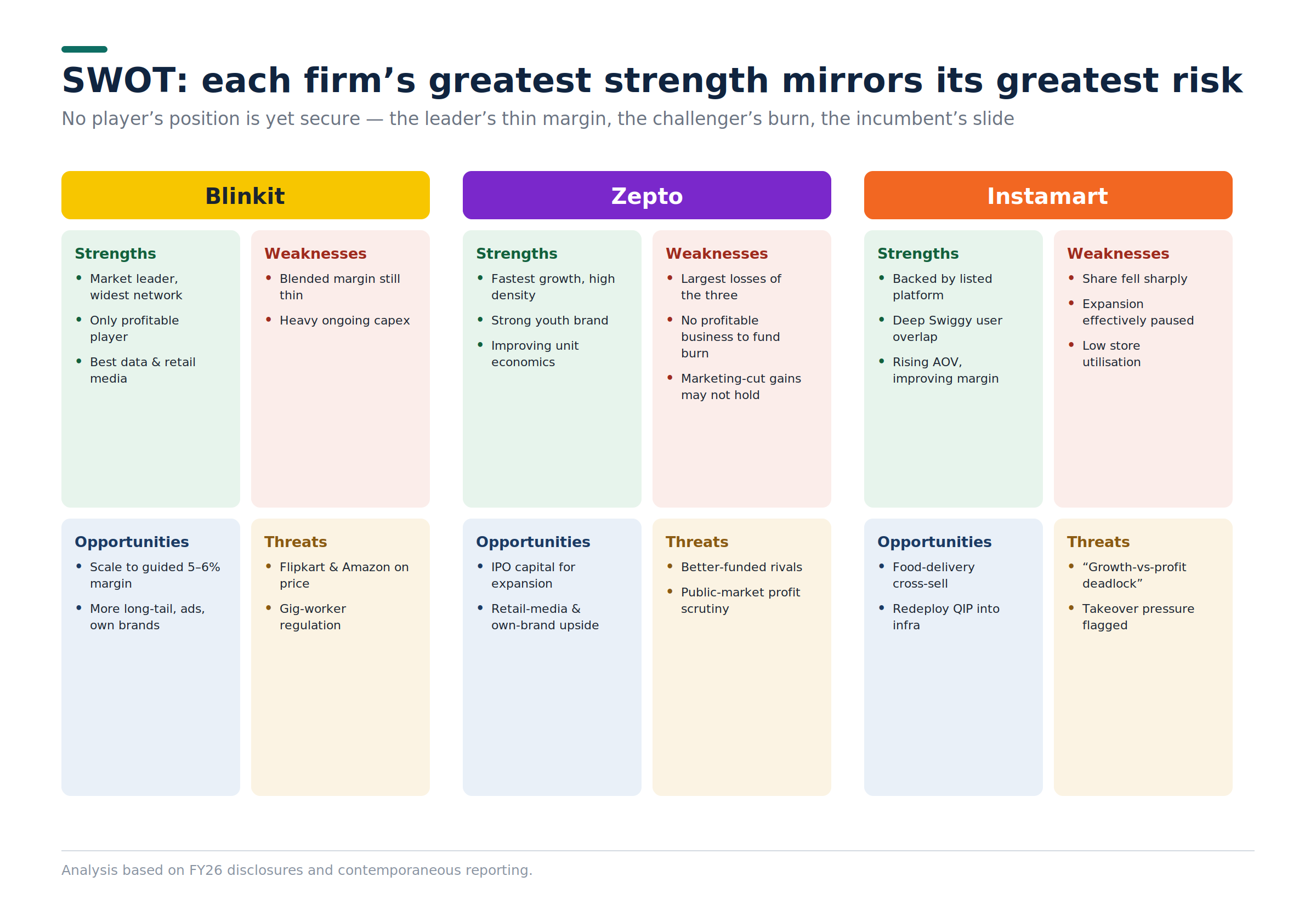

What does a SWOT analysis reveal for each player?

A structured SWOT shows that each company’s greatest strength is tightly coupled to its greatest vulnerability, which is why no player’s position is yet secure.

Blinkit

- Strengths: market leader with the widest, densest network; only player at adjusted EBITDA profit; best data and retail-media monetisation; funded by Eternal’s profitable food-delivery cash flow.

- Weaknesses: still-thin blended margin; heavy ongoing capex to hold the expansion pace; exposed to the price war started by new entrants.

- Opportunities: scale to a guided five to six per cent steady-state margin; expand into higher-margin long-tail categories; deepen advertising and private-label income.

- Threats: deep-pocketed Flipkart and Amazon competing on price; gig-worker regulation raising the cost to serve; category-wide discounting eroding margins.

Zepto

- Strengths: fastest growth and high order density per store; strong youth brand and trial conversion; pure-play focus and rapid product velocity.

- Weaknesses: the largest losses of the three; no profitable adjacent business to fund the burn; margin gains driven partly by a marketing cut that may not hold.

- Opportunities: IPO capital to fund density and category expansion; retail-media and private-label upside; status as the first listed pure-play brand.

- Threats: better-capitalised rivals in a capital-intensive game; public-market scrutiny of the path to profit; valuation compression if the growth narrative cools.

Swiggy Instamart

- Strengths: the backing of a diversified, listed platform; deep overlap with Swiggy’s food-delivery users; rising AOV and an improving contribution margin.

- Weaknesses: a sharp loss of market share; expansion effectively paused; the largest EBITDA drag on its parent; low dark store utilisation.

- Opportunities: cross-sell with food delivery and dining; redeploy raised capital into infrastructure; a private-label and margin-led turnaround.

- Threats: a growth-versus-profitability deadlock flagged by analysts; takeover pressure noted by some brokerages; two new large entrants competing for the same users.

Figure 11: SWOT Analysis: Blinkit, Zepto, Instamart

How do Porter’s Five Forces shape the industry?

Porter’s framework explains why quick commerce has been so difficult to make profitable: four of the five forces press hard against margins, and the industry’s attractiveness rests almost entirely on whether scale can overcome them. Rivalry is severe and intensifying, and the entry of Flipkart, backed by Walmart, and Amazon, both willing to sustain losses, has raised the threat of new entry sharply, because these are not startups but global giants with deep capital and existing logistics muscle.

| Force | Intensity | Why it matters for strategy |

|---|---|---|

| Competitive rivalry | Very high | Three funded incumbents plus two global entrants; metro capacity is already oversupplied, sustaining a price war. |

| Threat of new entry | High and rising | Flipkart and Amazon bring deep capital and logistics scale, neutralising the capital barrier that once protected incumbents. |

| Buyer power | High | Near-zero switching costs; multi-homing consumers chase the best deal, keeping discounting alive and margins thin. |

| Supplier power | Moderate | Owned inventory and private labels reduce brand leverage, but scarce gig labour and regulation raise delivery cost. |

| Threat of substitutes | Moderate | Kirana, scheduled e-commerce and planning ahead all substitute; instant delivery is attractive, not essential. |

Table 6. Porter’s Five Forces applied to Indian quick commerce.

Figure 12. Porter’s Five Forces in Indian quick commerce.

What does the future hold?

The most likely trajectory is a two-front future: continued margin improvement through automation and higher-value orders in mature metros, and a hard, capital-intensive battle for the next hundred million customers in smaller cities, ending in consolidation.

- AI and automation: moving from forecasting toward increasingly automated fulfilment and micro-fulfilment robotics, all of which lift the density flywheel and lower cost per order.

- Tier-2 and tier-3 expansion: the great growth question, where the density economics that make metros work are unproven, although Gen Z in smaller cities is adopting quickly.

- Path to profitability: Blinkit has shown it can be done; the contest is whether Zepto and Instamart can follow before capital or patience runs out.

- Private labels and higher-margin categories: beauty, electronics and general merchandise will grow as a share of baskets, lifting average order value and margin.

- Industry consolidation: analysts broadly expect the market to settle around two or three players as the cost of competing rises.

Figure 14. A two-horizon view of where the sector goes next.

What strategic lessons emerge for PGDM students and Future leaders?

The overarching lesson is that in a low-margin, high-frequency platform business, operational excellence and unit economics, not growth alone, are the true sources of competitive advantage, and every functional lesson below is a variation on that theme.

Strategy

- Growth without a credible path to profit is a liability, not an asset, a lesson public markets enforced by pressing Zepto to accept a lower valuation.

- Sustainable advantage comes from a reinforcing system, namely density that lowers cost, data that sharpens operations, and high-margin adjacencies such as advertising and private labels, rather than any single feature.

- First-to-profitability matters more than first-mover, which is why the leader’s discipline beat the pioneer’s head start.

Operations

- In thin-margin businesses, advantage is built from small, compounding operational gains and high utilisation; the density flywheel should govern expansion decisions.

- Controlling the supply chain, by owning inventory and forecasting demand at store level, converts a logistics cost centre into a margin lever.

Marketing and finance

- Buying customers with discounts inflates vanity growth but produces shallow loyalty; the durable prize is converting subsidised trial into habitual, full-price frequency, so lifetime value matters more than acquisition volume.

- Retail media and owned brands are how a thin-margin operator earns a real return; the most valuable revenue is often adjacent to, not identical with, the core transaction.

- Capital strategy is strategy: the ability to fund losses through a profitable parent, as Eternal funds Blinkit, can be as decisive as any product advantage in a war of attrition.

What is the enduring lesson of the quick commerce revolution?

Quick commerce has completed the journey from a marketing slogan to a structural feature of Indian retail, but the contest to own it is far from settled. FY26 delivered the first clear verdict. Blinkit demonstrated that disciplined scale can make the model profitable; Zepto demonstrated that audacious growth can build a formidable business that must now prove it can pay for itself; Instamart demonstrated that even a well-backed insider can lose ground when rivals compress the market.

For the student of strategy, the enduring value of this case is its clarity about what actually creates advantage in a platform business: not the speed on the label, but the economics beneath it. Whether the market ends with two national winners or three, the companies that survive will be those that turned ten-minute delivery from an expensive promise into a profitable system.

Related Blogs

How Reliance Jio Revolutionized India’s Telecom Industry: Strategic Lessons for PGDM Students

Summary This case study examines how Reliance Jio transformed India’s telecommunications industry within a few…

Pepsi Vs Coca-Cola: The Cola Wars and What They Teach Future Business Leaders

Summary The rivalry between Pepsi and Coca-Cola, widely known as the Cola Wars, is one…

How Titan Became One of the World’s Largest Watch Manufacturers

Summary This case study examines how Titan, a joint venture between the Tata Group and…

The Apple Comeback Under Tim Cook: A Business Case Study for PGDM Courses and Future Managers

Summary When Tim Cook became chief executive of Apple in 2011, many people doubted that…

UPI Case Study: How India Built the World’s Largest Real-Time Payment Network

How did a payment system built in India go on to process nearly half of…